Design and Evaluation of a Market Integrity Analysis System for Prediction Markets

Abstract

This project studies market integrity in prediction markets through a simulation and detection framework grounded in market microstructure and optimization. Prediction markets operate through event contracts that trade between zero and one, where the price reflects the implied probability of an event occurring. The reliability of this depends on sufficient liquidity, balanced participation, and resistance to strategic interference. In practice, those conditions are often not met, especially in thinly traded markets.

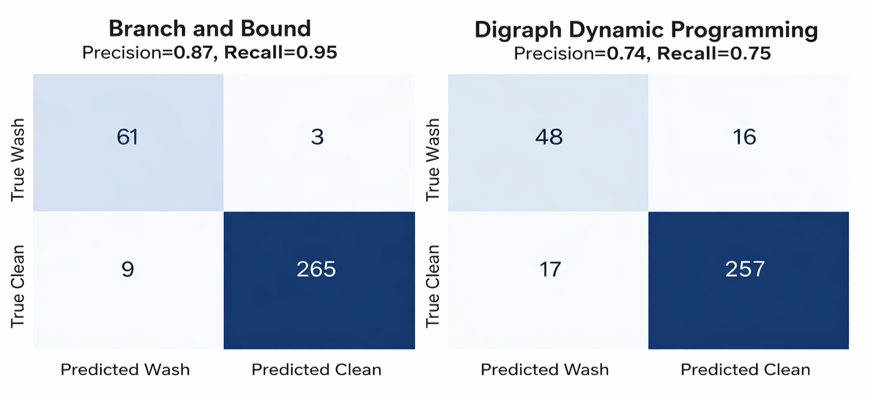

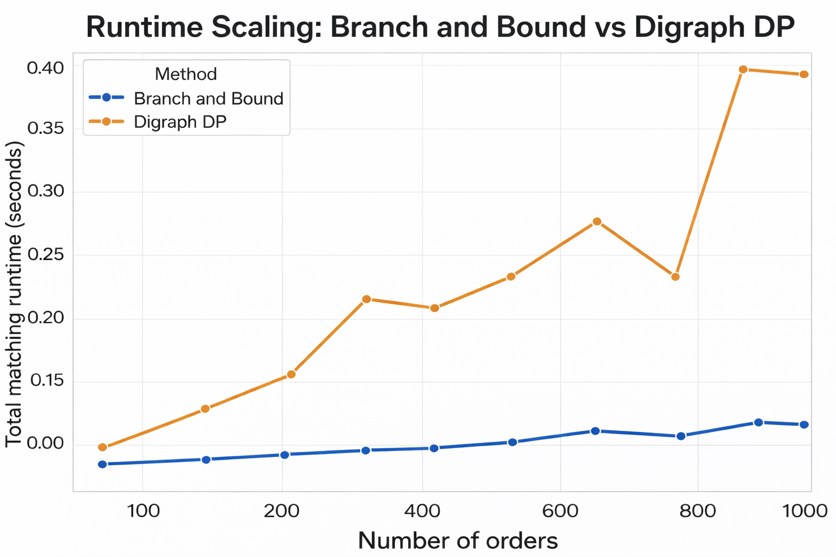

We developed a modular agent-based system using the Mesa framework, structured around a continuous double auction with a central limit order book. The system supports heterogeneous agents including noise traders, informed traders, and multiple classes of strategic manipulators. The central methodological focus is wash trading detection under a fixed structural formulation, comparing Dynamic Programming, Integer Linear Programming, and Branch and Bound. BnB achieves higher detection accuracy and computational efficiency relative to the other methods, with the pruning mechanism allowing large portions of the solution space to be eliminated early based on bounding conditions.

Background

Prediction markets have emerged as a mechanism for aggregating dispersed information into a single market signal through trading activity. Prices are interpreted as implied probabilities of future outcomes. Prior work has shown that prediction markets can perform competitively with, and sometimes outperform, traditional forecasting methods like polling or expert analysis.

Because these probabilities are observable and widely referenced in media, policy discussions, and strategic decision-making, they extend beyond purely financial relevance and can influence perception and belief formation. This creates a feedback loop where market prices don't just reflect beliefs but can also shape them.

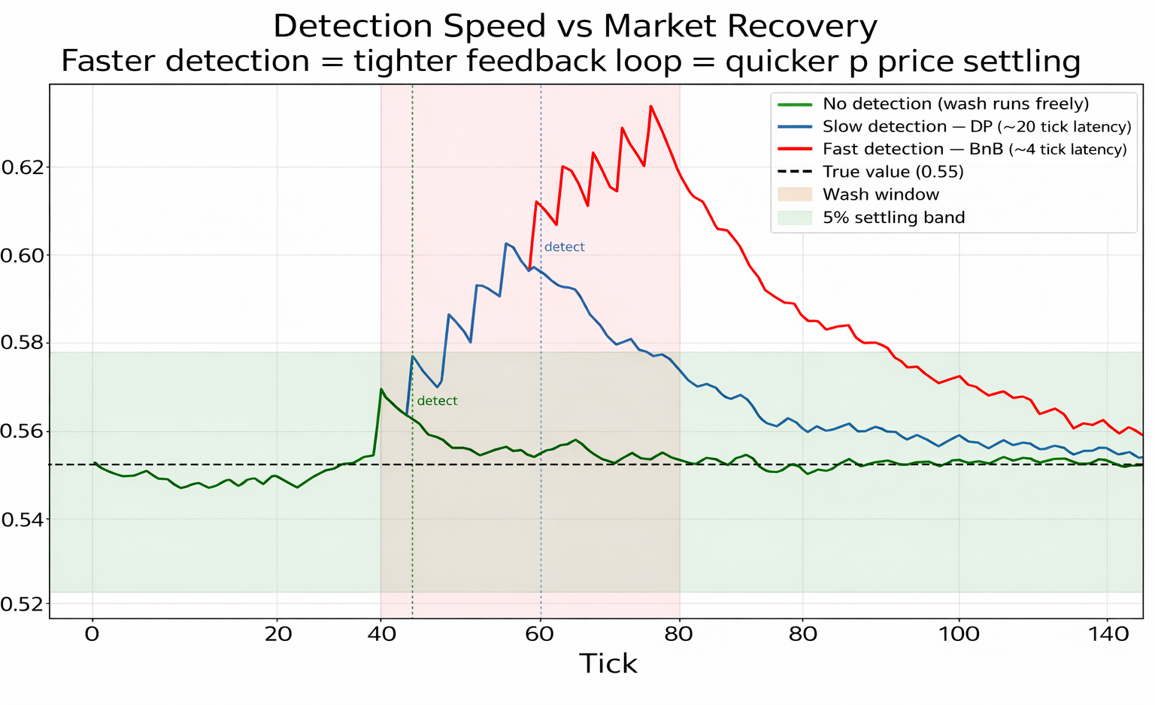

Manipulation risk is real. Rasooly and Rozzi demonstrated through a large-scale field experiment that prediction markets are manipulable, showing that even relatively small trades could produce price effects persisting up to 60 days. In low-liquidity environments, fewer counteracting trades exist to correct distortions, allowing manipulative behavior to have a stronger and longer-lasting effect.

Wash Trading

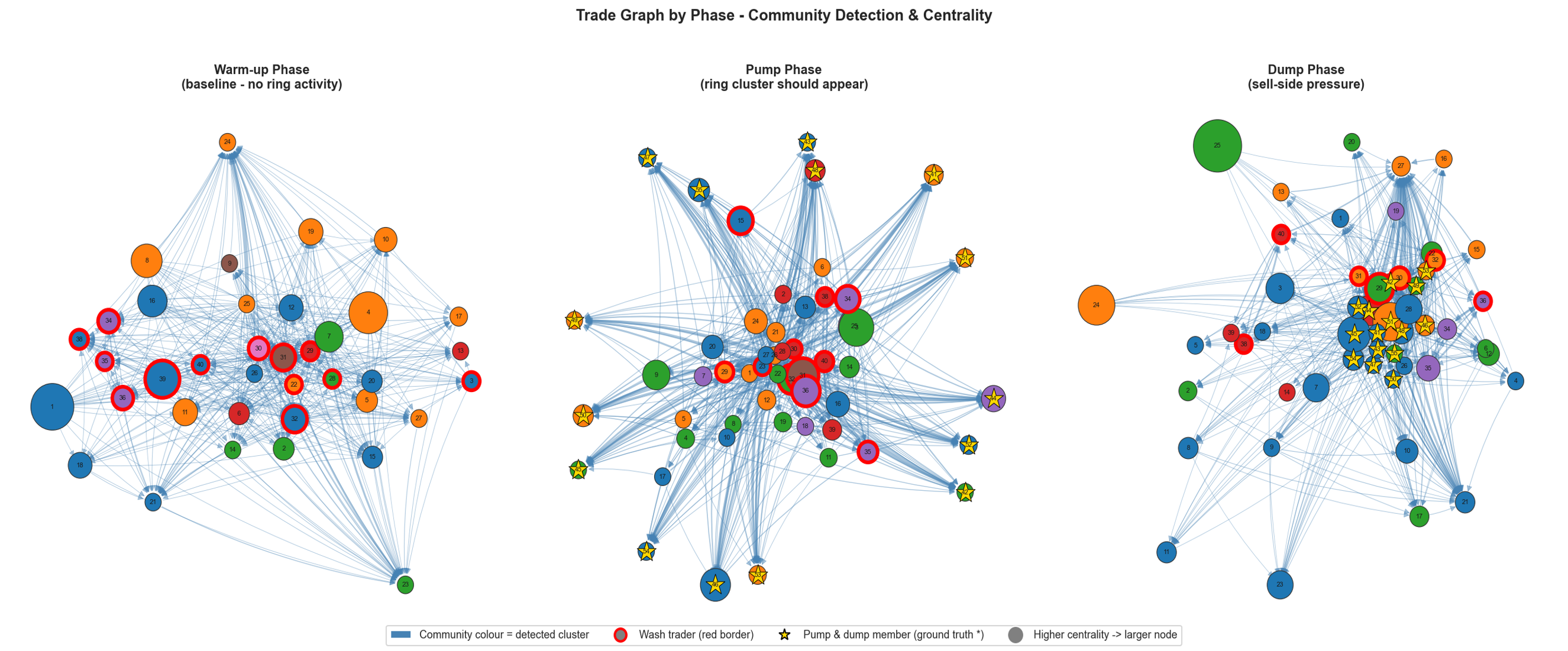

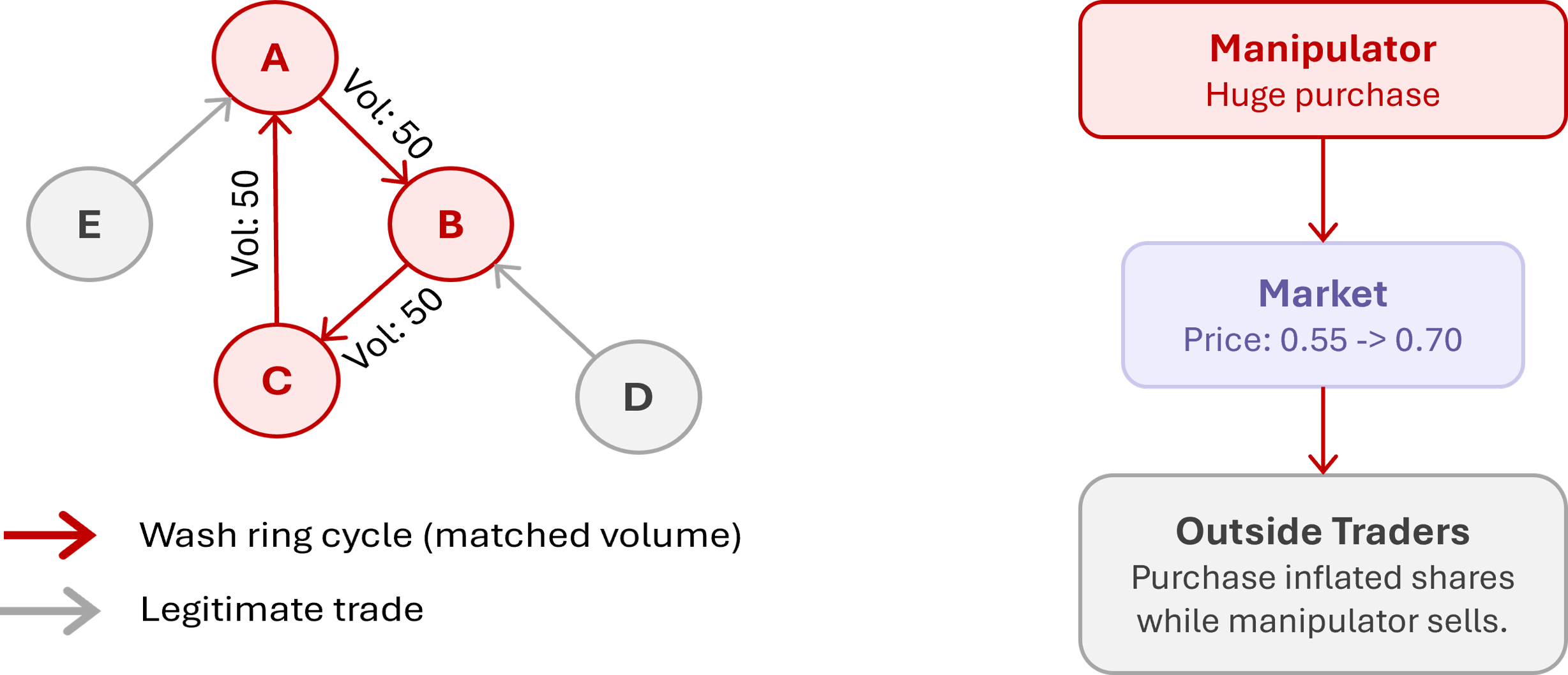

Wash trading operates through cyclic self-matching, where a set of colluding agents trade among themselves in a closed loop. Agent A sells to agent B, who sells back to A, inflating volume without any real transfer of ownership. A more complex variant involves coordinated ring structures where multiple agents form a directed cycle (A → B → C → A). No individual transaction appears suspicious in isolation, but the aggregate structure forms a closed flow of trades.

Pump and Dump

Whale distortion is modeled through a high-capital agent that initiates aggressive buy orders, driving the mid-price upward. This is followed by a reversal phase where the agent exits positions through sell orders once others have responded to the artificially elevated price. Unlike wash trading, which primarily affects volume and trade structure, whale-based manipulation produces a transient shock in price dynamics.

Methods

Agent-Based Simulation

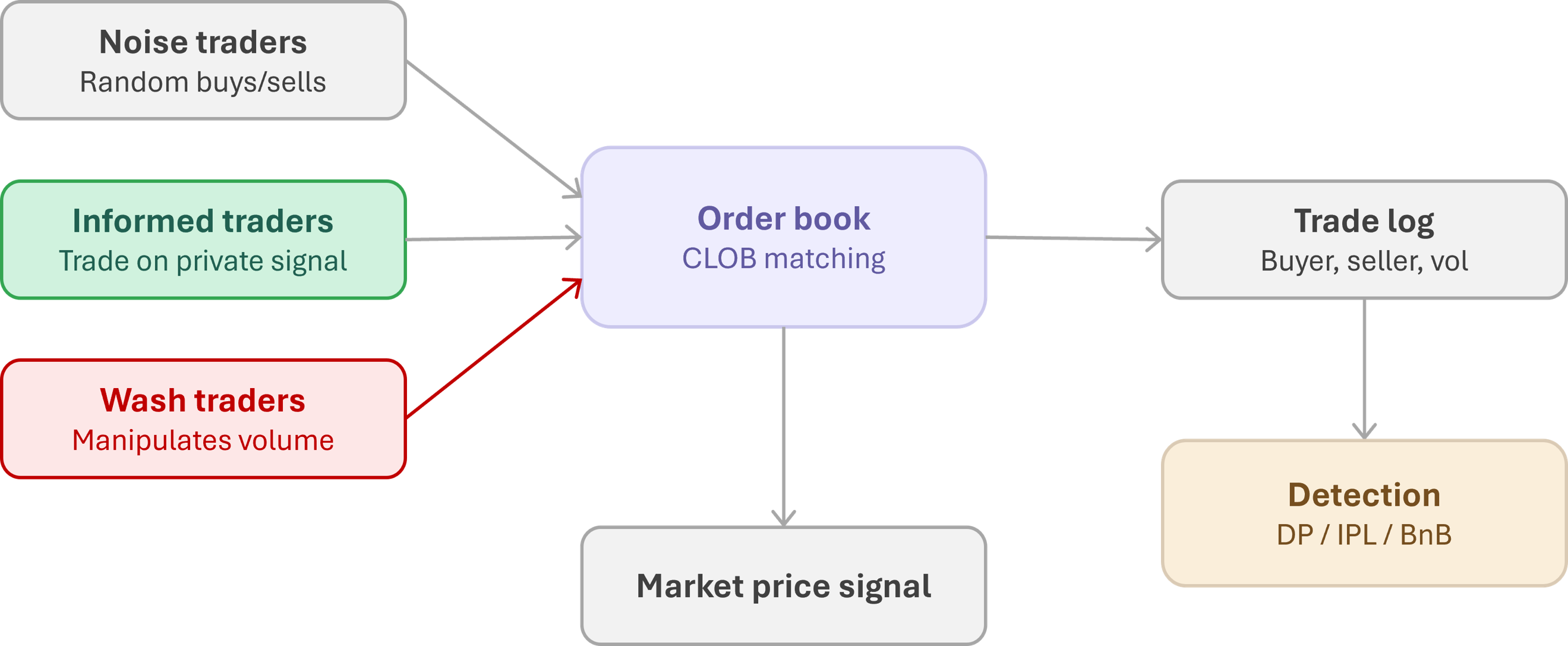

The market environment is implemented using Mesa, replicating a continuous double auction with a central limit order book. The CLOB maintains bids in descending price order and asks in ascending order. The matching engine follows price-time priority. Partial fills are supported. The simulation tracks all executed trades including price, volume, timestamp, and participating agents.

Digraph-Based Detection with Dynamic Programming

The detection framework is built on a digraph representation of trade flows where nodes are traders and directed edges are executed transactions. Wash trading is defined through two properties: trades must occur in tightly matched pairs satisfying constraints on time, price, and volume, and they must collectively form a closed cycle where total signed volume sums to zero. The subset selection problem is equivalent to a knapsack formulation. DP is the baseline, recursively constructing feasible subsets, but the number of possible subsets grows combinatorially.

Integer Linear Programming

The detection problem is re-expressed as an ILP. Each candidate trade gets a binary decision variable indicating whether it's selected as part of a wash structure. The objective maximizes total matched volume across selected trades. The core constraint enforces flow conservation: for each trader, the sum of signed trade volumes must be zero. This directly encodes the structural definition of wash trading from the digraph representation.

Branch and Bound

BnB is applied to the same subset selection problem. It traverses the search space as a decision tree where each level corresponds to including or excluding a trade. At each node, an upper bound on the achievable objective is computed. If this bound is less than the best solution found so far, the branch is pruned. In the implemented system, pruning is particularly effective because trades are pre-filtered based on tight constraints in time, price, and volume, which significantly reduces the number of feasible combinations.

Transient Response Analysis

When the whale agent injects a capital shock, the mid-price reacts like a dynamical system getting hit with a step disturbance. Three control theory metrics are used: overshoot (how far above true value the price gets at peak), undershoot (the drop below fair value during the dump phase), and settling time (how many ticks until the price stays within a 5% band around true value).

| Power Grid Concept | Market Equivalent |

|---|---|

| Steady-state voltage | Fair-value price (true probability) |

| Load disturbance / fault | Manipulation shock |

| Settling time | Steps until price returns within ε of fair value |

| Overshoot / undershoot | Max deviation above/below fair value after shock |

| System impedance | Price impact per unit manipulation pressure |

Timeline

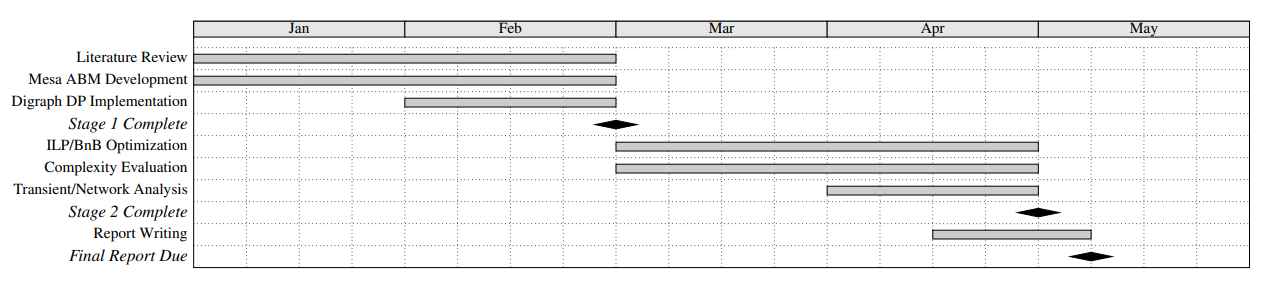

Stage 1: Core Simulation

Literature review, Mesa ABM development, CLOB/CDA implementation, digraph DP detection. Demonstrated computational limitations of DP approach.

Stage 2: Optimization and Evaluation

ILP and BnB implementation, complexity evaluation, manipulation regime design. BnB identified as only real-time viable method.

Stage 3: Analysis and Reporting

Transient and network analysis, report writing. Additional time allocated to refining BnB formulation and performance evaluation.

References

[1] Rothschild & Sethi, "Trading strategies and market microstructure: Evidence from a prediction market," J. Prediction Markets, 2016.

[2] Khodabandehlou & Zivari Hashemi, "Market manipulation detection: A systematic literature review," Expert Syst. w/ Appl., 2022.

[3] Cao, Du, & Tse, "Detecting wash trading in financial markets using digraphs and dynamic programming," IEEE CIFEr, 2015.

[4] Chen et al., "Gaming prediction markets: Equilibrium strategies with a market maker," Algorithmica, 2010.